Anime Financials 2016

While this site is meant to appreciate anime as an art, pretending it doesn’t exist as a business is a mistake. The industry is always a two-sided coin, and here is megax to unveil its performance over the last year. Enjoy!

Hello everyone and welcome to the start of hopefully a new annual tradition. Here at SakugaSakuga (作画): Technically drawing pictures but more specifically animation. Western fans have long since appropriated the word to refer to instances of particularly good animation, in the same way that a subset of Japanese fans do. Pretty integral to our sites' brand. Blog, we not only look at the names involved in animation; we also look at the names involved in producing/financing that animation as well. So I’d like to take the time and reflect back on the business side of animation in Japan in 2016. Most people only look at the estimates provided by Oricon, but there’s a lot more to the market than just home video releases. We’ll look at the increasing number of anime films, international rights payments, live event sales, as well as some other aspects of the industry in 2016 in this post.

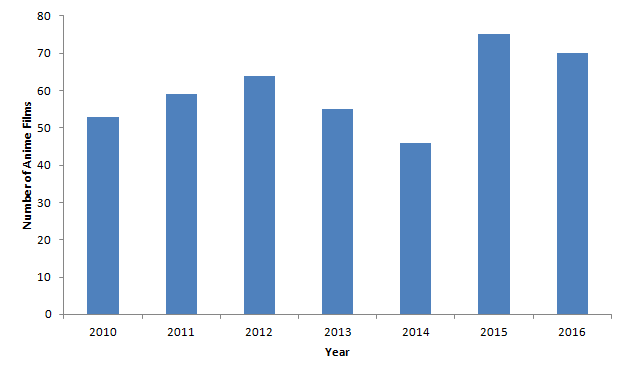

Anime films in 2016

The huge newsleader for 2016 was the sheer amount of yen at the box office, led by Makoto Shinkai’s Your Name’s record-breaking onslaught. Toho invested a good amount on advertising (and helped to widely place its trailer before many relevant movies, including their own hit Shin Godzilla) and gave it over 300 screens, by far one of the wider distributed anime films this year. However, the success at the box office doesn’t end with just Shinkai’s work; we saw a number of animated films perform admirably this year. One Piece Film: Gold set a national distribution record by opening on 743 screens and while it didn’t end up topping previous iterations of the franchise, it became another juggernaut that nicely accompanied Toei Animation titles like Precure that trended upwards in their yearly movie endeavors. This site will focus on Naoko Yamada’s new film, A Silent Voice, when it’s closer to a wide release in the West, but for now I’ll just say it earned over 2.3 billion yen this year. In This Corner of the World has been spectacularly carried week after week due to the excellent reception; from a very mediocre start to a respectacle amount, with a delayed release schedule that will probably allow it to reach over 1 billion yen (and has plans for an extended version as well). Though it was officially released last year, the sheer longevity of Girls und Panzer: The Movie has been a huge topic this year, reaching over 2.4 billion yen thanks to a ton of 4DX screenings.

For perspective, it’s rare for small run anime films that aren’t tied to family franchises (with around 120 theatre screenings) to earn over 1 billion yen, much less 2 billion yen. In addition, we saw releases of Kizumonogatari, Aniplex/Honeyworks’ duet of romance films, King of Prisim, Doukyuusei, KanColle, and many more smaller titles as well. The trend of using films in smaller theatre runs has been ongoing for years and doesn’t seem to stop anytime soon. We’ve already got many big titles like Sword Art Online, The Irregular at Magic High School, Fate/Stay Night: Heaven’s Feel, and many more titles lined up for next year. It’s easier to slot in a film or theatrical OVA in production schedules as well; they’re shorter in production length and time to produce animation/audio/sound/etc for. This spot will be something to keep an eye on for years to come. Bandai in particular seems to have moved towards theatrical OVAs as their preferred method of distribution, as seen on many of their flagship titles like Gundam and the sequel to the aforementioned Girls und Panzer.

So you might be asking “why has there been a shift to movies?” In short, it’s a much greater return for your finances. Not only do your customers have to pay to see it (unlike broadcast series), but you also have merchandise available for sale right there at the theatre for fans to buy. If you’re running a theatrical OVA in 5-24 theatres, you might have a theatre edition of the home video release (maybe with only 2.0 audio) for sale with a limited edition on sale later with all the whistles. Additionally, a 90-120 minute feature takes less time to produce and doesn’t require as much money going to all the various avenues of production (animation, music, sound effects, voice studio time, etc). While it’s annoying as international fans that we won’t get to see these works for a while, it’s a much safer avenue for the companies involved. Additionally, rights for films in Asia have been a big increase recently. Many of the films not shown in the west are licensed in Hong Kong/Taiwan and shown in theatres there. It’s not as commonly reported in the west because most news sites focus on English viewings, but that’s definitely a factor.

International Rights Sales

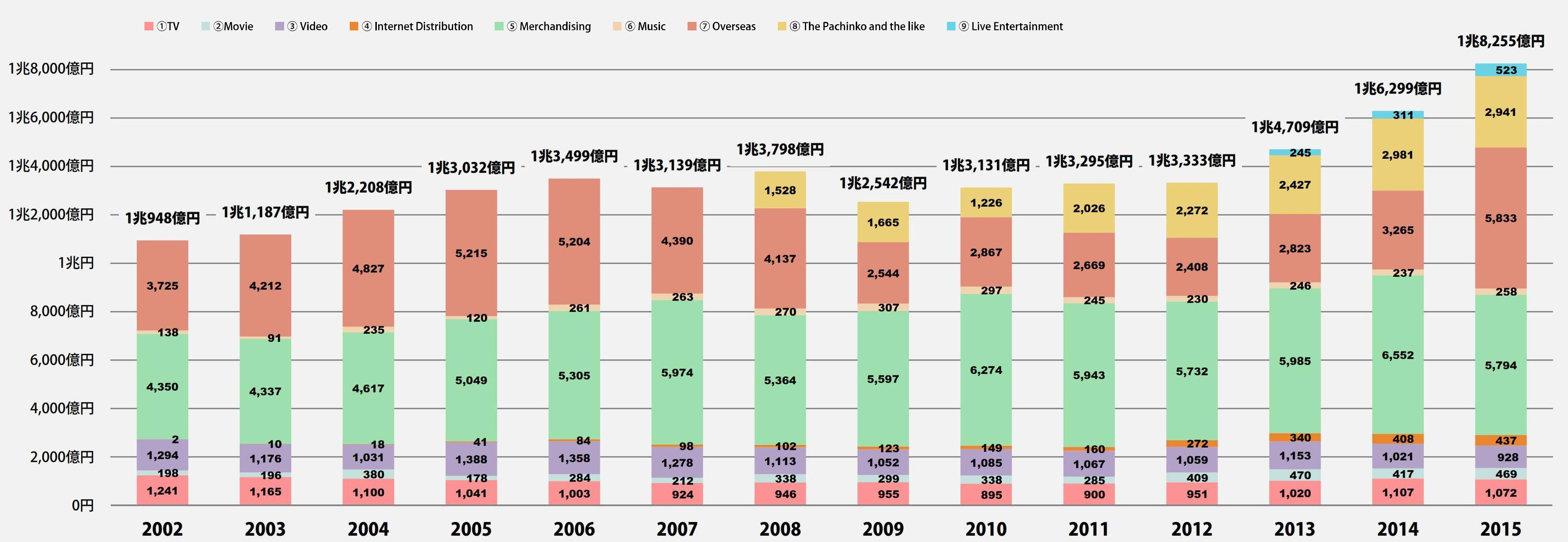

Another huge item for discussion has been the rise in international rights revenue. While this has been led by Chinese companies financing a lot of production costs (even going as far to produce many TV series themselves), the companies in the West have held their own. The combination of Crunchyroll and Funimation to share catalogs was a reflection of how costs have gone up for both companies and the necessity to focus on their own specialties (simulcast subs for Crunchy, dubbing/physical releases for Funimation). It’s a way to trim unnecessary costs for both companies as a result of licensing prices increasing. This isn’t all gloom and doom however. Crunchyroll has continued to increase their subscriber count worldwide to over 800,000 paying subscribers this year. That’s a lot of money coming in monthly to pay for new titles. With their focus on trying to increase regions for titles, I could see them becoming a small competitor to the Chinese companies (especially having served on committees as well). The Chinese boom has been both in streaming as well as films in theatres. In that respect, Crunchy actually does better getting a wider variety of content now (50 simulcasts this past season). With their funding, they’re actually one of the biggest producers of anime now.

Live Events Growth

One other area of growth has been in the live events sector. It’s becoming common to not only see an event ticket lottery code packaged in at least one or two home release volumes, but to see preview screenings (at least 1500 yen per ticket), fan events at places like Anime Japan, and other events in Akiba, Nagoya, and Osaka to celebrate releases of titles. All of this promotion drives sales of merch for shows and was the second biggest growth area of the industry in fiscal 2015 (and likely 2016 as well). This trend is helping video releases immensely. With tickets priced anywhere from 6000 yen to 12000 yen per ticket, plus event exclusive merchandise only sold there, we’re seeing this sector grow pretty strong. Will it be a bubble, or will we see things continue to grow here?

Digital Streaming (Japan)

Anime titles have been streaming online in Japan for years – don’t let anyone tell you differently because they’re not aware of companies like Bandai Channel, NicoNico, and d-animestore. However, we’re seeing more and more titles stream on many outlets now. I’ve seen many shows stream on around 12 services in one season; even a very niche project like Flip Flappers streamed on 18 different services last season, while a bigger deal like Yuri!!! On ICE was available on 21 streaming services in Japan alone. The biggest company that’s influenced this trend over the past year was Abema TV. It’s a free service that works similar to a TV channel with a few commercials during playback. We’re seeing a lot of new series stream weekly on it (or with marathons to catch people up). Some reports from certain producers (like at Pony Canyon and Warner Brothers) have the financials from streaming catching up to home video sales, but it’s not reached that level of revenue yet across the board. Despite that, Aniplex launched their own Viewcast streaming service that allows consumers to stream titles while on the go for titles they’ve bought the home video release of, like Kizumonogatari or The Anthem of the Heart; not only watch the titles themselves, but also have digital access to the extras such as production materials in digital form. This is another sector to watch in the future as consumers and businesses begin to focus on streams rather than rentals and eventually home video sales.

Mobile applications

One avenue that has had a lot of work carried out is mobile apps. In addition to things like Aniplex’s Koyomimonogatari (calendar story/Koyomi story) app and now Sword Art Online app, we’re seeing mobile developers on many committees now like i0plus, who served on Girlish Number’s, Izetta’s and Tawawa on Monday’s committee just this past season. This comes off a huge audience from Love Live using their game app. While I can’t speak to the financials of this as they’re not revealed, it’s definitely an area to watch for in the years to come.

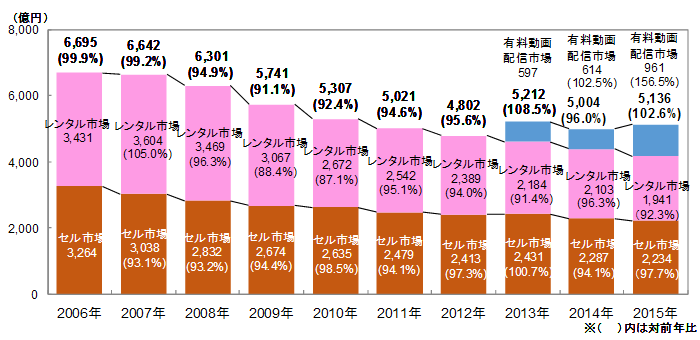

Home Video Releases

Finally, I’ll address the home video situation. While the numbers that are published weekly by Oricon are simply estimates of what was sold that week, it’s important to look at them as a trend. Unfortunately, that trend isn’t doing so well and it reflected in the fiscal 2015 numbers. 2016 was even worse outside of some very popular series. A lot of the titles that sold were bought primarily by women, and as a result, we’ve seen many more titles that were made with that audience in mind – though of course, intended demographics are always a relative concept, and all companies would like everyone to buy their product. Similarly, many publishers have started to move to a model of fewer volumes and more episodes per volume. Aniplex, Kadokawa Shoten, Media Factory, and Bandai Visual have released titles with anywhere from 4-6 episodes on a volume in 2-3 volume releases instead of 6 volumes with 2 episodes apiece on them. The prices are equivalent per episode for both, but it’s fewer releases for the consumer. It’s not as if physical latenight anime releases are getting cheaper (contrary to western opinion, this has already been attempted to unsatisfactory results) but the delivery might change. This method is something to keep an eye on next year. Will it continue or will they go back to singles for everything again?

While disc sales are not the end-all-be-all that some people think, they do contribute a lot of revenue to a project. This decrease in the revenue from this source is not a good sign. The market is shifting, so we’ll have to see what other avenues pick up the slack. More movies? More focus on streaming? More focus on international rights? More merch? Only time will tell.

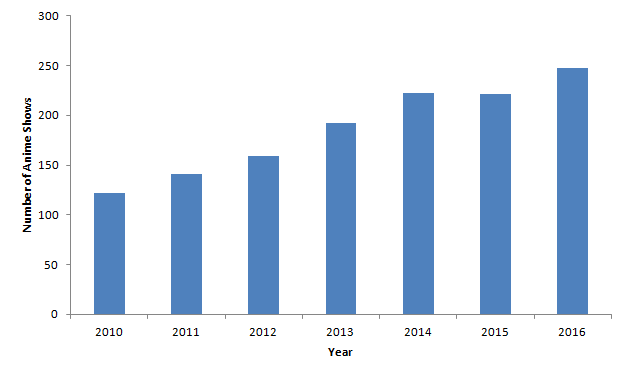

Increasing Number of TV Anime

One consequence of this shifting market away from home video releases as the main source of income for late night shows has been in the sheer number of productions pushed out this year. We’ve seen many more productions fall behind this year compared to normal due to rushed scheduling by producers leading to subpar broadcast products. The obvious recently examples are Actas’s productions and Brave Witches, all of which have had episodes delayed due to how far behind schedule they got. Obviously, this isn’t healthy for the market and I expect we’ll see a contraction in the number of productions either next year or the year after as it shifts to regain some stability (perhaps with films since they’re shorter to produce). Otherwise, we’ll see a lot more stressed production managers.

Conclusion

In conclusion, we’ve seen the continuation of market shifts in 2016 from last year. It’s an exciting time to watch how the finances of each production have shifted in response to things like declining home video sales/rental sales and towards streaming. Looking at the committees this year, I continued to see a lot of diversity in production financing (meaning a lot of companies on various shows like Flip Flappers and Yuri!!! On ICE), which is minimizes damage. Splitting the risk of a show over multiple companies means that a loss wouldn’t affect one as badly as it would with a smaller committee. Will we see that next year? Again, we’ll have to wait and see. Overall, things are still looking good for the future of anime. The companies involved in financing productions are finding ways to earn their money back, and more shows do indicate a lot of support somewhere. While there are some worrying points (are we past the amount that can be done at the same time?), I’m much more hopeful after seeing the rise of international rights money this year compared to last year.

Have a safe and Happy New Year to you all!

Sources:

- Lists of Japanese Anime films in the 2010s.

- Association of Japanese Animation Data.

- Japan Home Video Association 2015 annual report.

- Gem Standard 2015-2015 streaming video prediction report.

Support us on Patreon so that we can keep producing all this content and fullfill our next goals, as well as affording all server expenses. Thanks!

I enjoyed this article, but I feel it’s omitting the fairly important aspect of anime adaptations, especially TV anime, as a means of promotion for their respective source material. Chihayafuru S1 posted awful sales numbers, but the uptick in manga sales was so substantial the whole endeavor was considered enough of a success to get the band back together for a second season.

The challenge there, in my experience anyway, is that data is even harder to make sense of than the anime data. Our available reporting options for games, novels, and manga omit a vast swathe of the market due to the sheer number of releases and very high thresholds to even rank. And even if AJA/JVA-style reports exist for these industries, you’d need to separate out the ones that have anime adaptations from the ones that don’t. There’s no “Novels with Anime Adaptations” industry report out there. The lack of good series-level data (as opposed to these very broad topline numbers)… Read more »

As someone who regularly tracked boosted sales of original manga/LNs for quite a while, I feel *THIS ENTIRE COMMENT*. Not to say there was no worth in that, it worked as a general gauge and some cases were extreme enough we could determine their success or failure without further context, but for the most part it was painfully incomplete. Print reports are a nightmare unless they come from official sources, and even then they tend to ignore the sometimes very significant digital sales. Having no knowledge of their expectations is also a dealbreaker very often, since there’s no universal success… Read more »

Kodansha, the manga publisher for Chihayafuru, was not on either committee. They explicitedly refused to be on one, which forced VAP’s and NTV’s producers to fund both anime seasons themselves. Manga sales did not matter at all for it, so using it as an example of “it was just made for promotional sake!” is hilariously incorrect. I chose not to include information on manga/novels in this post because that’s an entirely seperate industry. The Japanese publishing world is much larger than what we see in the West, especially when it’s limited to titles that have been adapted into anime (and… Read more »

Isnt the increasing number of tv anime deceptive? There have been, seemingly, more short (14, 11, 7, 5, even 3? minute) anime being made. Surely production managers cant be falling behind on those or even falling behind on shows pushed to online services (like Monster Strike, unless that had a tv airing?)

No for two big reasons:

-The minutes of animation produced have also increased, that’s also tracked data (understandably, since plenty of people already wondered if the trend towards shorter series canceled that out). Obviously not proportionally with the insane increase of number of titles, but strongly up nonetheless.

-Even ignoring that, more productions is in and of itself a very important piece of data. Under similar circumstances, two 1 cours anime are more costly than one 2 cours anime – twice the preproduction costs after all. It would still have an impact on the industry.

Is this the correct “minutes of animation” chart from the AJA 2016 (i.e. 2015 data) summary report? http://i.imgur.com/fapUDsx.png (Page 5 of the report. I have a downloaded copy saved but can’t find the actual URL.) If so I minutes decreased in 2015, even if we’re well up from the recent 2010 low point. And we’re still a good bit below the 2006 peak, albeit higher than any point from 2000-2005. Do we have 2016 minutes yet? There’s a bunch of explanatory text on that chart I can’t parse. but I think it may be saying kids/family anime plunged pretty far… Read more »

Source 2 above should be the report you’re talking about. It points out that around 120,000 minutes is about the limit of animation that can be produced per year. 2016 numbers will be out around the end of next year as this report is published around October-November. Again, this doesn’t count the amount of time needed for pre-production. More new shows mean more time spent planning how the series will go plot-wise, getting designs ready, getting setting designs ready, getting plot designs ready, etc. Sequels don’t need /as/ much time unless you’re in a new setting and/or have a lot… Read more »

Additionally, that is TV minutes; part of the difference between 2014 and 2015 was due to more productions moving to theatrical formats instead, which had by far their peak of minutes produced in 2015 (it’s on the other graphs in that report). Usually you can’t say project X existing doesn’t influence Y, but in this regard… yeah it definitely does. Staff, studios and companies that were restricted to TV series before no longer are.

Really fantastic insight! This is the exact kind of content that I want more of(other than sakuga analysis and other production related stuff, of course!) Are there any specific examples of the cheaper physical releases that Japan experimented with? I see this stated a lot, and believe it, but I don’t think I’ve ever actually seen an example of one of these “reasonably” priced Japanese releases that did really poorly. I’ve imported a ton of stuff, and have a lot of releases from Japan that weren’t particularly expensive, but most of them are budget boxes that came out years and… Read more »

Something like GJbu is a good example, since it’s not the kind of show that would traditionally aim to have a cheaper release because of more mainstream targets – though it was distributed by VAP, so it’s easy to understand why that of all shows was chosen. 4 volumes, each of them quite cheaper than normal BDs. In the end, a bit over half prince of a “normal” 1 cours show… and it still averaged only about 3k copies, which doesn’t really feel like double the people who’d have bought it at regular price.

Yeah, that seems like a good example. Ideally you’d want a bunch more than just double as well. haha

Doubt that show would’ve set the world on fire, but about I could’ve seen it getting 3k even with normally priced sets.

Great article! Many usefull informations.

Little sad, that there’s no mentions for the studios who are in difficulties (Hello Gainax), or closed their doors in 2016 (Hello Manglobe and Fantasia).

Ho, and I was not aware that the home video market has tempted a shift in the past, when was-it and what was the shift? price dropping/more complete box?

Anyway, thanks for the hard work.

‘Studios struggling’ could be a post on its own… though not the most cheerful thing to write about, to be honest. Also you can’t pinpoint any modern attempt at changing pricing en masse, more like a bunch of individual attempts that didn’t seem to go well so they didn’t lead to anything. The current move towards more box-like (though still with multiple volumes) releases is the biggest deal we’ve seen in a long time, and even then it’s sloooooow.